- Love and other assets, by Plenty

- Posts

- When saving is costing you

When saving is costing you

Emily Luk, CPA, CFA and CEO of Plenty

August 25, 2024

Love & other assets Vol. 18

When saving is costing you

Dear Plenty Community,

Welcome back to the Love and other assets: 2 x 1 x 1 newsletter.

Last newsletter, we talked about how stocks are meant to be held over longer time periods - volatility in Japan and a soft jobs reports now seem to be last year’s news as the market had an 8 day boom and is hovering around all-time highs again. For those who panic sold in the drop, they’d probably have missed out on the recovery - lesson: staying with it makes your return, and emotion-driving buying and selling is often the reason why average traders (including wallstreet traders) average a ~3.6% return while the market (aka S&P500) averages 9.5% - source: JP Morgan.

In this week’s 2 news moments, we’re doubling down on Google. The Department of Justice is considering breaking up Google. We’ll talk about why and how it’s come this far, then give a quick economics 101 tutorial on why democratic governments care about competition.

In our deep dive this week, we look into the aftereffects of the robinhood covid trading boom, the tech bust, then the two years of high interest rates. All of these tipped the scales to consumers saving more than investing and creating a financial reality where…

Saving might be costing you

Aja Dang joined us on this week’s Love and other assets. We talked about her paycheck routine to make planning effortless, what “just makes sense” for managing joint and personal accounts as a child of divorce, and how she saved her way out of hundreds of thousands of dollars of student loans.

As always, if you have ideas or questions you’d like us to answer, write in to [email protected] - I’d love to hear from you.

Cheers,

Emily

For those that are new: 2 x 1 x 1 means

2 news moments in business/finance to keep you in the loop

1 deep dive to help you and your partner with money

1 tidbit for your relationship

TWO: MOMENTS IN THE NEWS TO KNOW

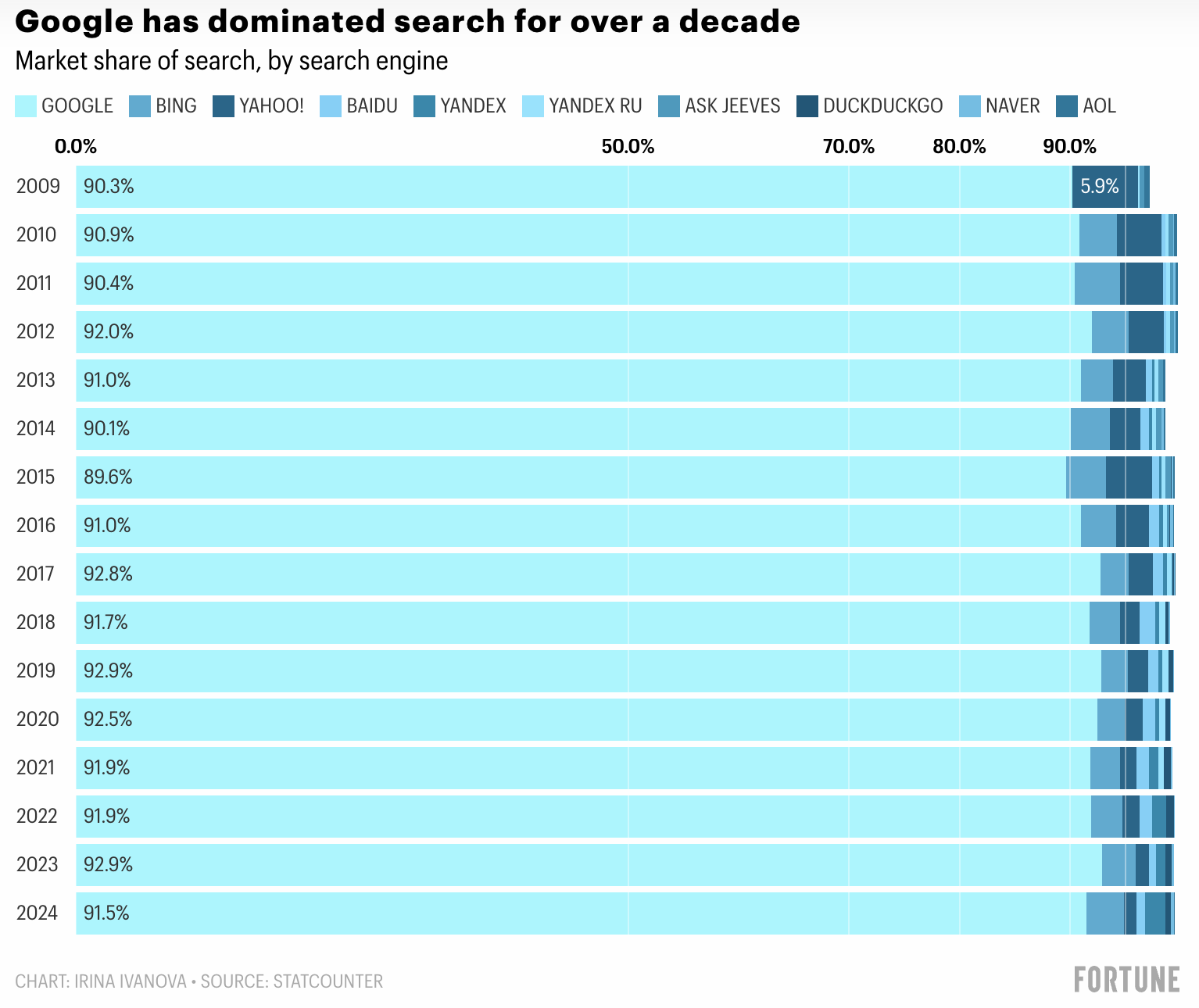

Google’s officially a “monopoly” and might be broken up

As Google has grown and outcompeted Yahoo, Bing, and countless other search engines, Google has heavily invested in growing a legal team to fight lawsuits that might label the company as a ‘monopoly’. After two decades, Google just lost in federal courts for the first time. Google’s primary revenue stream has long been advertising revenue through its search engines.

As they’ve looked to grow their reach, they’ve invested billions into preferred placement of Google via Chrome browsers on a growing range of devices like Samsung or Apple phones. The Department of Justice has successfully proven a monopoly over search ad placement at the top of the search results. Google lost almost $300B in value as markets speculate over what the DOJ may decide as potential remedies.

Why we care about monopolies

Economic theory and what we’ve typically seen is that monopolies are bad for everyday consumers. When companies compete with another company, they’re pushed to improve the quality of their product and their prices. Here’s an easy example: imagine you moved to a new neighborhood and there was only 1 coffee shop within a 60 minute drive. Even if the quality of their coffee got worse, you wouldn’t have another option and you might go anyway.

Imagine if a 2nd coffee shop opened across the street: the original coffee shop is now more likely to think deeply about the quality of their coffee, whether it’s more or less expensive, whether the shop ambiance is inviting compared to the new shop, and so on. Where a government starts to become concerned is when there are business practices that prevent competition: imagine if that original coffee shop could pay landlords to not allow any other coffee shop to open in the town. As a local, you might not have much power to do anything and that’s where governments are meant to step in.

ONE: FROM THE PLENTY BLOG

When saving is costing you

I was raised to save: to be responsible, put my money aside, and save money for future me. In a world where parents often repeat the importance of “being careful” and we’ve never learned when risk is a good thing, this has resulted in a savings pile up that is costing Americans. And time is not on our side.

I’ve done it too - the more stressed I am, the safer it feels to have a growing pile of cash. When I first started my career in the early 2010s, we had mostly recovered from ‘08. Everybody kept talking about how we were about to go through another recession (we didn’t). So I didn’t invest initially. ‘Recession’ has been a newsworthy topic every year for almost 15 years now. The safe path might be costing you more than you realize.

ONE: FOR YOUR RELATIONSHIP

The one question to strengthen your relationship with

“What can I learn about my partner?”

Dr. Orna Guralnik has seen a lot - “There’s too much emphasis nowadays on a kind of solipsistic, self-absorbed way of approaching the world. We see that between couples. My attitude is, it’s exactly the opposite thing we need. We need to listen better, not argue better for our own needs.” The one thing more couples can do, is to stay open to their partner. Focus on what you can learn from them.

LOVE & OTHER ASSETS

On this week’s episode

Aja Dang gets real about her journey from YouTube to becoming a finance guru. Her top advice? “Just start.” She admits she was scared to dive into things like saving or paying off debt, but once she did, it made all the difference. Aja opened up about her $150,000 student debt, which hit home for a lot of people because, let’s be real, "someone's finally talking about debt."

When it comes to managing money with her husband, Aja takes the lead and she makes sure they’re taking care of shared needs in joint accounts and personal needs/wants in individual accounts. She also learned the hard way that saving more than 20% for a house is a must, and lifestyle changes are no joke. Through it all, Aja’s all about being flexible and figuring out what works best for you. Her message? “Take control and start living the life you want—because you totally deserve it.”

ABOUT PLENTY

Plenty is a wealth platform helping modern couples invest and plan for their future together. We bring the investment strategies and products of the wealthy to the everyday household. Plenty was started by a husband and wife team dedicated to growing together. For more information, visit withplenty.com. If you ever have any feedback or questions, please do reach out to us at [email protected].

At Plenty, no financial topic is off-limits for modern couples. We offer straight talk and judgment-free guidance to help modern couples navigate the tricky and important intersection of money and relationships. Join thousands of couples who’ve signed up for our free newsletter today.